American Outperformance in the Global Economy

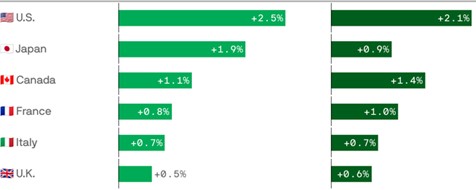

The economy and markets in 2024 performed amazingly well in the U.S. particularly in relation to the rest of the world. This performance gap has been persistent over time. Europe, for example, continues to fall behind the U.S. in terms of growth and productivity. Between 2010 and 2023, the cumulative growth rate of GDP reached 34% in the U.S. compared to just 18% in the eurozone. Over the same period, labor productivity grew by 22% in the U.S. versus 5% in the eurozone. Our economy rebounded quickly from the pandemic and the challenges of the past four years, and the Federal Reserve Board has done a competent job in bringing down inflation. The Personal Consumption Expenditures (PCE) Index has gone from 8% in 2022 to a little over 3% in 2024. The Federal Reserve Bank of New York estimates that the PCEI inflation is currently running around 2.25%.Moving forward, how sustainable is U.S. productivity growth, profits and business investment in the economy? It is true the 10-year Treasury yield has risen quite a bit, but a lot of the rise has been in real yields, not inflation driven. As we’ve pointed out in a previous quarterly letter, rates were abnormally low, and current levels are more reflective of long-term historical rates.

GDP Growth Among G7 Nations

Moving forward, how sustainable is U.S. productivity growth, profits and business investment in the economy? It is true the 10-year Treasury yield has risen quite a bit, but a lot of the rise has been in real yields, not inflation driven. As we’ve pointed out in a previous quarterly letter, rates were abnormally low, and current levels are more reflective of long-term historical rates.

The economy is not without challenges ranging from the deficit to geo-political conflicts, China and the new administration’s fiscal and trade policies. One of the first hurdles facing the new Congress and administration is the growing deficit and size of the federal debt. The U.S. gross national debt keeps expanding at an exponential rate and has reached $36 trillion. Secretary of the Treasury, Janet Yellin, in late December warned the U.S. could reach its debt ceiling as soon as mid-January. If the average rate of debt growth continues at this pace, the debt held by the public will reach a record level of more than 106% of Gross Domestic Product, breaking an almost 80-year record set in 1946 when the U.S. was recovering from World War II, according to a recent Congressional Budget Office forecast.

Of particular concern is the rising cost of servicing the debt and its potential impact on yields. Interest payments on the national debt totaled more than $1.2 trillion for the government’s fiscal year ending in October. The interest payments alone in 2024 exceeded the entire historic deficit in 1945, even after adjusting for inflation. Net interest payments are now the third costliest item in the budget behind Social Security and Medicare benefits. Indeed, interest payments surpassed U.S. military outlays for the first time in history. As recently as 2012 defense spending outstripped interest payments by threefold.

The U.S. economy has always faced challenges, but it also has proven to be durable and flexible, and the Fed has demonstrated its commitment to using its tools to fulfill its dual mandate of promoting maximum employment and price stability.

Other trip wires include ongoing global conflicts with wars in Ukraine and the Middle East that can destabilize the global economy. China is struggling to maintain its target growth and its managed economy has built-in vulnerabilities and bubbles (e.g., real estate) from previous attempts to stimulate its economy.

The incoming Trump administration’s fiscal and trade policies could prove inflationary, creating headwinds for the Federal Reserve. Promises of across-the-board tariffs, tax cuts and curtailing immigration could serve to increase the cost of labor and goods.

The U.S. economy has always faced challenges, but it also has proven to be durable and flexible, and the Fed has demonstrated its commitment to using its tools to fulfill its dual mandate of promoting maximum employment and price stability.

The U.S. is the undisputed leader in artificial intelligence, which could be a source of longer, stronger productivity. The Trump administration is already modulating its policies from a campaign posture to a governing one. There are several policy options to reduce the deficit although some are politically unpopular. Reforming entitlement programs offers the most realistic path toward reducing the deficit and reining in the national debt. In the past, delegating reforms to an independent commission has been the vehicle to depoliticize an issue and move toward a realistic path to modest reform. In addition, since the end of World War II, the U.S. dollar has enjoyed a privileged status as the world’s most important currency for international trade and financial transactions. This position has been beneficial for the U.S., providing price stability and lower interest rates compared to the rest of the world.

There are certainly risks on the horizon to economic stability, such as the deficit, but there are also scenarios for improvement. The bottom line is that, for the time being, investors around the world continue to regard the U.S. as a sound economy in which to invest with independent, stable and robust institutions and a free enterprise system that is flexible and adjusts to the ever-changing business cycle.

Company Comments

Comments follow regarding common stocks of interest to clients with stock portfolios managed by Delta Asset Management. This commentary is not a recommendation to purchase or sell but a summary of Delta’s review during the quarter.

Avery Dennison Corporation (AVY) is the leading manufacturer of pressure-sensitive labeling materials. The company is also one of the world’s largest producers of retail apparel ticketing and branding systems, radio frequency identification (RFID) inlays and tags, and specialty tapes. Avery has a significant global presence with approximately 200 manufacturing and distribution facilities in 50 countries and product sales in 89 countries. More than 70% of revenue is derived from international markets, including emerging markets.

The company maintains a dominant market share position in its two main businesses: pressure-sensitive materials and retail branding and information solutions. Avery’s specialization – superior product offerings and effective customer service – should continue to strengthen its relationships in these businesses. Although both business segments have reached maturity in developed markets with pockets of excess growth remaining in specialty labels and RFID tags, Avery continues to build on its already significant emerging markets presence. In the long term, these economies are expected to see a growing demand for packaged goods, and similarly, the demand for apparel will also rise. In addition to adding new regional partnerships, Avery grows as its multi-national customers expand into new, faster growing regions.

Avery’s size affords it a manufacturing scale advantage. The company’s scale enables it to achieve operating efficiencies that generate a premium profit margin over its competitors. Further, its multi-year operating improvement plan has successfully grown company profitability to record levels. The firm’s extensive global distribution network and long-standing customer relationships further strengthen its advantages over its competition, particularly with large consumer products manufacturers, such as Procter & Gamble. These relationships can be “sticky” due to the tailored servicing involved. Meeting specific customer specifications and formats increases switching costs.

The Materials Group, which includes pressure-sensitive materials, is Avery’s most important business segment and contributes 70% of company profits. Avery is more than twice the size of its nearest competitor. The company’s technical and engineering expertise continues to lead to innovative new products, such as thinner, more flexible labels that conform to oddly shaped consumer packages and bottles. Avery’s latest innovation includes linerless label solutions that reduce customer waste and improve efficiency and sustainability. These specialty labels are a faster growing segment of the market with premium operating margins. The technology is important to consumer products manufacturers for brand awareness and product appeal on the shelf.

We expect Avery will continue to benefit from the use of RFID tags, which are rapidly growing and have become an increasingly important part of the overall company. RFID tags contain data that helps companies manage their inventory and distribution. Avery dominates this space with annual revenue expected to continue to grow 15% or more going forward. Growth in web shopping and omni-channel retailing will continue to drive rapid growth for RFID inlays due to its inventory management and supply chain advantages.

Given Avery’s exposure to mature markets, innovative labeling solutions and its increasing market share in faster-growing emerging markets, we have assumed the company can grow revenue approximately 4.5% annually over the next decade. At this pace, given the company’s operating efficiencies partially mitigated by competitive pressures, we believe cash flow margins can average approximately 15.5% during this period. Based on these assumptions, our stock valuation model indicates Avery’s current price offers a long-term average annual rate of return of almost 8%.

Founded in 1897, Becton Dickenson and Company (BDX) is one of the leading medical device companies supplying a diversified mix of basic and sophisticated products throughout the world. In recent years, the company has made two transformative acquisitions: CareFusion in 2015 and C.R. Bard in 2017. The integration and benefits of the acquisitions have been larger than expected. The company has extracted cost synergies while maintaining the culture and expanding the portfolio of products. The acquisitions helped transform the company from a commoditized medical supply and devices manufacturer into a healthcare solutions company that improves healthcare processes and efficiencies.

Most of Becton’s sales are in what are called “sharps,” which consists of safety needles, ultra-thin pen needles, hypodermic needles, syringes, catheters and related equipment. The company maintains the largest market share of sharps worldwide based on the quality of its products, innovation, world-wide service capability and lower cost. Expansion opportunities remain in foreign markets due to slower adoption of safety guidelines and the need to minimize the spread of infectious diseases in developing countries. The essential and recurring nature of Becton’s medical products allows the company some relative stability in revenues despite the tougher medical technology spending environment. We expect this business will continue to generate strong free cash flow, which management has historically deployed wisely.

Legacy CareFusion is a global leader in medication management and delivery and in patient safety solutions. CareFusion focuses on medication management, infection prevention, operating room and procedural effectiveness and respiratory care with a large installed base of equipment and high switching costs. CareFusion maintains the No. 1 market position in many of its product categories, especially in infusion pumps and medication dispensing equipment, where it is estimated to hold 25% and 70% global share, respectively.

The C.R. Bard segment has a leading product portfolio in the areas of vascular, urology, oncology and surgical specialties. The products include bioresorbable grafts, vascular stents, vascular grafts, angioplasty balloon catheters and IV filters. Bard is strong in urology and has a suite of new solutions to help streamline medication management.

Becton’s other businesses are more technology oriented and also have large market shares. The primary products are diagnostic testing instruments for disease detection and cellular analysis instruments for pharmaceutical and biotech research. Both product categories have related equipment and supplies businesses that are sizeable. Cost pressures and lab technician shortages are driving demand for automation, while increased access to healthcare in emerging markets is driving the need for both automation and disease screening.

Becton is truly a global company with researchers, clinical labs and manufacturing located outside the U.S. The company generates almost 60% of its revenue internationally with 20% of its customers in emerging markets, well ahead of the industry.

In June 2024, Becton announced it is buying Edwards Lifesciences’ Critical Care business specializing in cardiovascular catheters, sensors and monitors all which complement Becton’s product categories. These products will be exposed to Becton’s broader geographic footprint and distribution.

Hospital buying groups are consolidating to increase their purchasing power with suppliers. Longer term, the major risk to Becton is the commoditization of sharps, which Becton continues to combat through innovation, such as safety-engineered devices and ultra-thin pen needles. In addition, Becton faces growing competition from medical product manufacturers with sizeable research budgets, particularly in fast-growing segments. In healthcare there is always the risk that competitors create more innovative products that disrupt the industry by replacing existing products.

We feel confident assuming higher growth in Becton’s more innovative businesses, such as diagnostics and drug dispensing technologies, with more modest growth in its maturing needle business. The population of the world is growing, and in major industrialized nations it is aging, which implies medical equipment will be in strong demand. Based on these assumptions, our stock valuation model indicates Becton’s current stock price offers a long-term average annual rate of return of approximately 9%.

The Walt Disney Company (DIS) is a global, diversified entertainment company with operations spanning theme parks, broadcast and cable television, movie production, consumer products and new online video streaming services. The company owns some of the world’s most valuable media brands including ABC, Disney, ESPN, Lucasfilm (Star Wars), Marvel and Pixar. Disney’s broad media and entertainment breadth provides diversified distribution channels for the company’s creative content. Over the last several years, Disney has focused on three key strategic priorities: creating high-quality content for the entire family, making that content more engaging and accessible using technology, and growing its brands and businesses in markets around the world.

The strength of Disney’s media brands is solidly in place and will continue to provide the company with opportunities to create high-quality content and experiences for years to come. The company has been extremely adept at using brands and creative content to generate revenue and profitability through multiple sales channels.

The COVID-19 pandemic resulting in a new stay-at-home paradigm has helped drive viewers to the Disney+ video streaming service, making it a viable player in the first year of its launch. The service was a success even before the pandemic. Streaming will benefit from the new content being produced at Disney and Fox Broadcasting, along with their film studios and extensive franchise libraries.

Disney has focused on three key strategic priorities: creating high-quality content for the entire family, making that content more engaging and accessible using technology and growing its brands and businesses in markets around the world.

Sports are Disney’s major content edge. As consumer viewing options expand (internet and mobile media) and become more fragmented, and as viewing preferences change, “must see” live sports provide ESPN with an advantage over traditional cable distributors and advertisers. ESPN continues to profit from cable affiliate fees, and it generates revenue from advertisers interested in reaching adults ages 18 to 49, a key advertising demographic that watches more sports and less scripted television than other groups.

Disney’s theme parks have recovered to pre-pandemic levels in terms of attendance. In addition to the wholly owned domestic parks, Disneyland and Disney World, the company has partial ownership and management contracts to operate several international parks in France, Hong Kong, Tokyo and now China. Disney has invested heavily over the past few years in adding new attractions, new resorts and new cruise ships as well as park expansions and upgrades. Disney theme parks are one-of-a-kind destinations that have competition, but nothing with the scale, magnitude, uniqueness or relevance for the entire family as the Disney experience.

Disney does face long-term challenges. The cost of sports programming rights continues to rise sharply, and ESPN pays handsomely to acquire major sports contracts. ESPN has been able to defray some of these costs by charging ever-increasing affiliate fees to cable operators. With such high fees, angst is growing among viewers, cable operators and program competitors. If ESPN cannot continue to pass along sports rights costs to cable operators, its profit margins will erode; however, profit erosion would be gradual due to ESPN’s long-term contracts with both major sports leagues and cable operators. The high value of sports has also created additional competition for ESPN. All major broadcasters, such as FOX and NBC, and the major sports leagues have increased their investments in sports programming. More competition for viewers is likely to drive up the overall operating costs to broadcast sporting events over time.

Disney is transitioning from a media industry driven by traditional television networks and cable distributors to one reliant on streaming services. Disney+ and Hulu have reached large enough scale to become profitable. The sizable content inventory Disney owns should provide flexibility for how the industry evolves – whether through individual subscriptions or a greater use of bundled packages.

Robert Iger returned to the role of CEO in November 2022 after previously serving as CEO from 2005 to 2020. He is set to retire in 2026, and the company has yet to announce his successor. In the meantime, the company named Morgan Stanley veteran James Gorman to be Chairman. He served as CEO of the Wall Street bank for 14 years and has experience in succession planning and transitions.

Disney’s proven ability to develop entertainment icons with increased consumer opportunities from merchandising royalties, positive cable pricing, theme park expansion and new film and online TV streaming services should allow the company to continue its good revenue growth with solid operating profit margins. Our valuation model suggests that the company’s stock is priced to generate a long-term average annual rate of return of approximately 9%.

Comcast Corporation (CMCSA) is the nation’s largest cable provider offering a range of information, entertainment and communication services to residential and commercial customers. The cable segment’s network is complete with video, high speed internet (HSI) and voice as well as digital video and wireless services that can be accessed by 62.4 million homes and businesses in 39 states with 31.6 million domestic residential customer relationships. The company’s NBCUniversal Media business is a leading entertainment and media company that develops, produces and distributes news, sports and entertainment for global audiences.

Comcast’s cable segment is mature, with subscriptions for video declining and broadband growth slowing. As a result, the firm has shifted focus to increasing average revenue per unit (ARPU) served. This change is achieved by capitalizing on the speed differential with periodic price increases and bundling.

Comcast’s cable segment is mature, with subscriptions for video declining and broadband growth slowing. As a result, the firm has shifted focus to increasing the average revenue per unit (ARPU) served. This change is achieved by capitalizing on the speed differential with periodic price increases and bundling services.

A critical Comcast defense is its industry-leading internet speeds. With the continuing shift toward online and mobile video and gaming, internet speeds are vital to continuing to drive growth in its high margin HSI business. Comcast continues to add over one million customers per year to its HSI services. Data consumption growth continues to increase the importance and value of Comcast’s faster pipe into homes and businesses. Comcast’s network architecture allows it to add capacity to meet customer speed demands at a far lower cost than competitors. In addition, Comcast Business services continue to be a high margin growth driver for the company.

Comcast’s NBCUniversal has experienced a turnaround. Comcast has improved this collection of businesses, which includes cable networks, NBC broadcast stations, movie studios and theme parks, to provide adequate growth and good cash flow. Comcast is investing to transform the entertainment unit into a compelling multi-media juggernaut with the parent company’s ample capital, scale and digital know-how. Its central focus will be sports and top echelon theme parks. With investments in NASCAR, NCAA football, NFL football, the Olympics and Premier League soccer, it is betting it can boost fees and advertising. Sports are “must see” live events, whether at home or digitally while on the go, and still command premium ad rates.

The company has rolled out a new streaming service to compete in the direct-to-consumer market. The service, named Peacock, has access to a vast library of popular content such as Friends, Seinfeld and The Office as well as new original content and live sports such as golf, NASCAR, NFL and Premier League Soccer. In July 2024, the NBA negotiated new broadcast rights agreements, which included Comcast’s NBC. The agreement will run for 11 years beginning with the 2025-2026 season with Comcast reportedly paying $2.45 billion a year for its rights, which is representative of the increasing cost of content that distributors are experiencing.

Comcast has positive attributes including recurring, predictable cash flows and competitive advantages, such as substantial scale and a fully built-out network. The significant capital investment needed for a new entrant to build a competing network serves as a barrier to entry and limits the ability to compete on price. With its network complete, Comcast can add new subscribers and improve the speed and capacity with only modest additional costs, while increasing the overall return on investment.

Competition is intensifying for broadband customers as telecom companies expand into Comcast service territory with competing networks. AT&T is reinvesting in fiber expansion and plans to reach thirty million households by the end of 2025. Comcast estimates that 50% of its footprint faces fiber competition today, increasing to 60% in the next couple of years.

The company has several responses to the various competitive threats it faces; however, we believe it is prudent to expect modest revenue and earnings growth over our forecast horizon and reduce our exposure given Comcast’s maturing businesses. Our stock valuation model estimates a long-term annual return for Comcast of over 9% based on its current stock price.

December 31, 2024

Specific securities were included for illustrative purposes based upon a summary of our review during the most recent quarter. Individual portfolios will vary in their holdings over time in relation to others. Information on other individual holdings is available upon request. The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy. The opinions expressed are subject to change from time to time and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. Any projections are hypothetical in nature, do not reflect actual investment results and are not a guarantee of future results and are based upon certain assumptions subject to change as well as market conditions. Actual results may also vary to a material degree due to external factors beyond the scope and control of the projections and assumptions.